Payslips are an important document to understand. It sets out what you have earned and what you will be paid. Sometimes they are a little hard to understand, so to help you, we’ve worked through an example.

About Paradigm Norton: We look at money and financial planning from a different perspective. We help you face planned and unexpected change, using your wealth to help you realise your life’s goals.

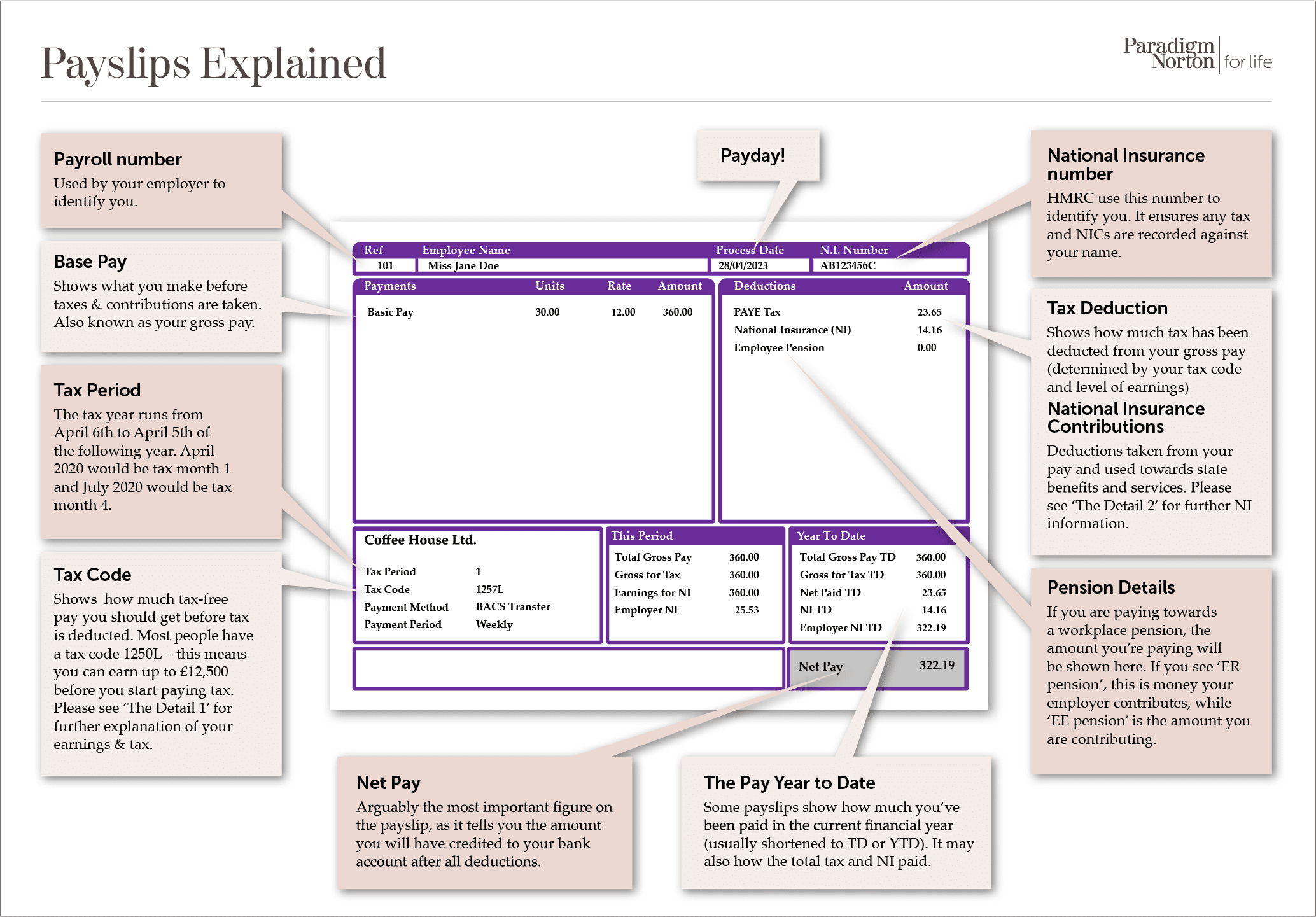

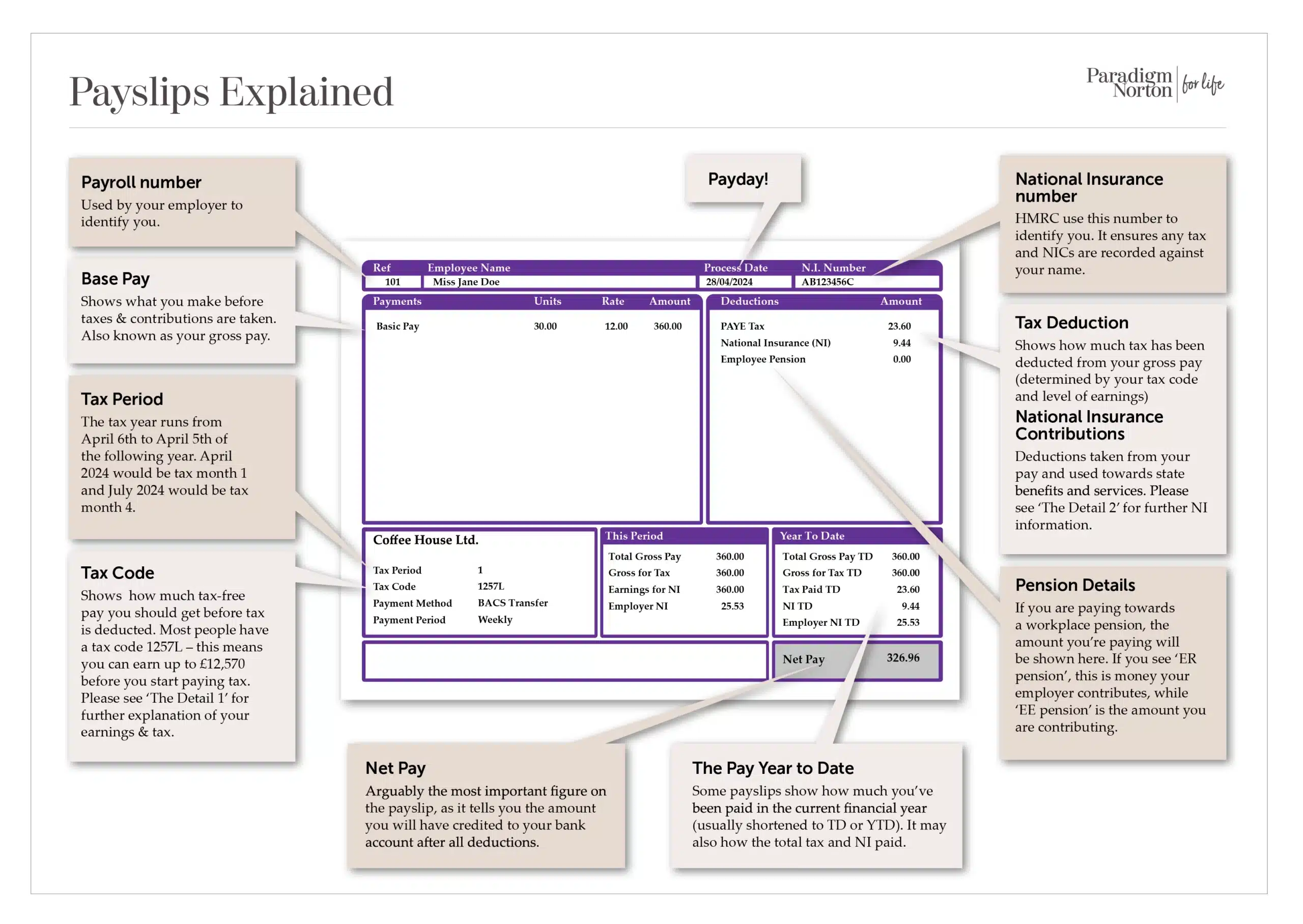

Your payslip details explained

Payroll number: Used by your employer to identify you.

Base Pay: Shows what you make before taxes & contributions are taken. Also known as your gross pay.

Tax Period: The tax year runs from April 6th to April 5th of the following year. April 2024 would be tax month 1 and July 2024 would be tax month 4.

Tax Code: Shows how much tax-free pay you should get before tax is deducted. Most people have a tax code 1257L – this means you can earn up to £12,570 before you start paying tax. Please see ‘The Detail 1’ for further explanation of your earnings & tax.

Net Pay: Arguably the most important figure on the payslip, as it tells you the amount you will have credited to your bank account after all deductions.

The Pay Year to Date: Some payslips show how much you’ve been paid in the current financial year (usually shortened to TD or YTD). It may also show the total tax and NI paid.

Tax Deduction: Shows how much tax has been deducted from your gross pay (determined by your tax code and level of earnings)

National Insurance Contributions: Deductions taken from your pay and used towards state benefits and services. Please see ‘The Detail 2’ for further NI information.

Pension Details: If you are paying towards a workplace pension, the amount you’re paying will be shown here. If you see ‘ER pension’, this is money your employer contributes, while ‘EE pension’ is the amount you are contributing.

What is tax and who pays?

Tax is the way the Government raises much of the money the country needs to pay for the things that we all benefit from, such as schools, hospitals and roads. There are many forms of tax, but the one we’re going to look at here is income tax.

As soon as you start to earn over a certain amount of money each year, a proportion of that money is paid to the Government via their tax collection agency Her Majesty’s Revenue and Customs (HMRC). The amount paid to the Government is known as income tax.

Explore: Tax Planning Services.

When you become employed, your employer will automatically deduct the income tax from your earnings and send it to HMRC. (If you were self-employed, i.e. working for yourself, you would be responsible for paying the income tax you owe directly to HMRC.)

The personal allowance

Each year, nearly everyone can earn up to a certain amount of money that is free from income tax. This is known as the personal allowance. In the tax year 2024/25 – which runs from 6 April 2024 to 5 April 2025 – the personal allowance is £12,570.

The personal allowance generally goes up each tax year and its existence means that those on relatively low incomes, including those who work part time while in full time education, do not typically pay any income tax.

For example, if you were to earn £12,000 a year, you will not pay any income tax because your income is below the personal allowance of £12,570. The personal allowance will reduce, partially or completely, for those earning over £100,000.

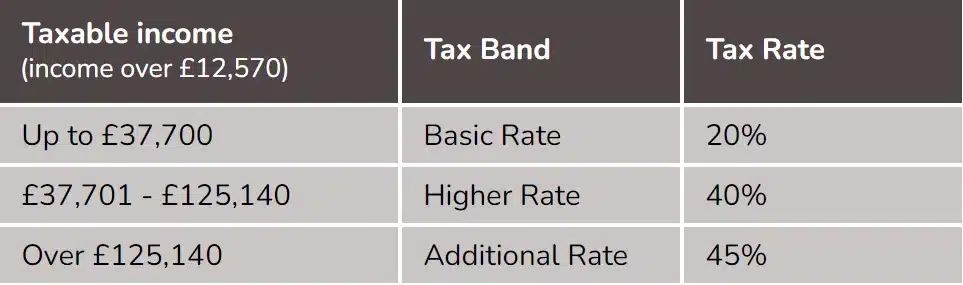

The tax bands

UK income tax is a progressive tax. This means that the Government takes more money from those who earn more, than they do from those who earn less. Income in excess of the personal allowance is known as taxable income. It is taxed as follows:

For example, if you had a full-time job and started earning £28,000 per year, you’ll pay income tax as follows:

-

- First £12,570 – no tax, as this will fall within your personal allowance

- Next £15,430 (£28,000 minus the £12,570 personal allowance) – taxed at 20% as this will fall within the basic rate band

Therefore, the total tax bill would be £15,543 x 20% = £3,086

Pay As You Earn (PAYE)

The UK operates on a Pay As You Earn (PAYE) system, which is essentially a method of paying tax and National Insurance contributions (NICs) during the year. Your employer withholds taxes due from you from your pay, before paying you your wages. At the end of the tax year, you will receive a form, known as a P60, which outlines the total amount you were paid for the previous tax year along with any deductions.

National Insurance is a tax on earnings paid by both employees and employers. Your National insurance contributions (NICs) are taken from your earned income and used to pay some state benefits. National Insurance payments go towards state benefits and services, including:

- The NHS

- State Pension

- Unemployment benefits

- Sickness & disability allowances

You’ll need to pay into National Insurance for a set number of years to be entitled to receive the state pension. If you haven’t met the minimum amount of contributions, you may not qualify for some benefits.

How much National Insurance do I pay?

Unlike Income Tax, National Insurance is not an annual tax. It applies to your pay each period (which may be monthly or weekly). The National Insurance contributions (NICs) will be taken off along with Income Tax before your employer pays your wages. You begin paying National Insurance once you earn more than £242 a week (for the 2024/25 tax year).

The amount you pay depends on how much you earn:

- 8% of weekly earnings between £242 and £967

- 2% of weekly earnings above £967

For example, if you earn £500 per week, you pay:

- Nothing on the first £242

- 8% (£19.36) on the next £258

Do I need to keep my payslip?

Payslips provide an important record of what you have earned and how much tax you have paid. At the end of the tax year you will receive a P60 document which provides a summary for the year, but the individual documents are still important.

Your payslips can help prove how much money you earn each month. This might be helpful if you are applying for a mortgage, or need to claim a means-tested benefit. For this reason you might be asked to show several months of payslips to establish a pattern.

HMRC recommends that you keep your pay and tax records for at least 22 months after the end of the tax year. So for the tax year which ended on 5 April 2024 you should keep those documents until at least February 2026.

Important notes: The information is based on our understanding of current taxation, legislation and HM Revenue & Customs practice for the 2024/2025 tax year. The tax treatment depends on the individual circumstances of each individual and may be subject to change in future. The Financial Conduct Authority does not regulate tax advice.